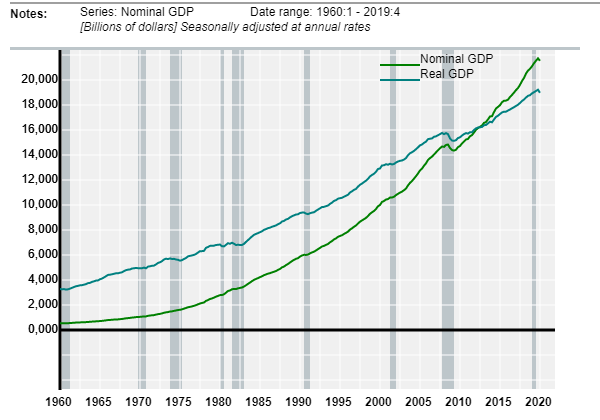

As can be seen in the above numbers, what appears to be solid economic growth (4% per year in NGDP) may be largely due to inflation and the corresponding change in market values. Over the past fifteen years, in real terms, Real GDP in the U.S. has been growing on average by 1.8 to 2.2 percent annually.

2.2.3 Business Cycles

Business cycles are recurring changes in the level of business and economic activity over time. This business activity is measured via measures of Real Income specifically Real GDP.

Quite often these cycles occur because spending in the economy (as measured by RGDP) differs from the ability of the economy to produce goods and services. A prolonged period of growth in spending that exceeds the growth rate in output will lead to tight factor markets. The economy may transition into a period of decline (recession) simply because the current rate of spending cannot continue.

One business cycle is defined as a period of economic decline or a contraction followed by a longer expansionary period.

A Business Cycle A period of economic expansion followed by a contraction in real GDP followed by another expansion. A business cycle is measured peak-to-peak.

These cycles occur at regular intervals in a market economy as the rate of real economic growth exceeds the growth in the potential of the economy to produce goods and services. As resource limits are reached in an expansion; credit is restrained, the cost of borrowing increases, and resource prices begin to rise. All of these factors put a squeeze on the profit margins of business firms which often leads to a curtailment of business activity.

Recessions may also occur or be prolonged as consumers and producers become more pessimistic about future economic events. This pessimism may lead to a decline in both consumption and investment spending resulting in an increase in inventory levels. Businesses respond to this unanticipated increase in inventory through cutbacks in production and the corresponding layoffs of workers.

Business cycles are characterized by expansions or continued increases in Real GDP followed by contractions or a decline in Real GDP. The transition from expansion to contraction is called a business-cycle peak. These contractions or recessions are officially defined as two or more quarters of negative growth in Real GDP. The transition from recession to the next expansion is known as a trough in the business-cycle. A full business cycle is measured from the peak of one cycle to the peak of the following cycle .

2.2.4 The Output Gap

A more accurate description of cyclical economic activity would be with respect to long run trends. This trend is defined by growth in the Potential Output of the economy 'Y*'. Growth in output depends on growth in the availability of factor-inputs (labor, materials, capital energy) and changes in technology. It will rarely be the case that Real GDP 'YR' will grow at exactly the same rate as potential output. Instead, it is more likely that due to demand-side shocks (changing expectations, changes in economic policy or, changes in the global geo-political situation), Real GDP will vary about the potential of the economy.

The difference between Real GDP and Potential Output is known as the Output Gap:

When Real GDP exceeds the potential of the economy to produce, an Inflationary Gap is the result. This growth in spending is leading to depletion of inventories and tight factor markets as producers rush to replenish these inventories by hiring more inputs. These tight factor markets lead to higher factor prices and, depending on the degree of competitive pressure that exists in a given industry, higher prices to the customers of these products. If Real GDP is below the potential of the economy, a Deflationary Gap exists. In this case there is little upward pressure on factor or output prices. However, the economy is not operating to its full potential such that living standards are lower than what otherwise be possible.

2.2.5 A History of Business Cycles (business cycle dating)

Since World War II, most business cycles would last 3-5 years peak-to-peak. The average duration of an expansion was 44.8 months and the average duration of a recession has been 11 months. By comparison, the Great Depression which saw a decline in economic activity between 1929 and 1933, lasted 43 months peak-to-trough. The Great Recession of 2008 - 2010 also represented a more extreme and prolonged decline in output.

Post War (WWII) Recessions

Time Period, (length) -- Reason

1945 - 1945 ( 8 months) -- Post W.W.II transitions

1948 - 1949 (11 months) -- Inter-war adjustments.

1953 - 1954 (10 months) -- Transition from the Korean War

1957 - 1958 ( 8 months) -- Ike's Rolling Readjustment

1960 - 1961 (10 months)

1969 - 1970 ( 8 months)

1973 - 1975 (16 months) -- Oil price shocks, breakdown of the Bretton-Woods fixed exchange-rate regime, and perhaps the end of the Viet Nam War.

1980 - 1980 ( 6 months) -- Second oil price shock and the "Energy Crisis"

1981 - 1982 (16 months) -- Recession induced in part by the Federal Reserve's reaction to the buildup of inflationary expectations of the 1970's

1990 - 1991 ( 9 months) -- End of a long peacetime expansion and perhaps perhaps induced by the burden of debt accumulated in the 1980's and triggered by the Gulf War.

March 2001 - Jan. 2002 -- End of the 'Irrational Exuberance' in financial markets that emerged in the late 1990's and a built up of excess capacity in the telecommunications sector.

December 2007 - June 2009 (19 months) -- the Great Recession, the Financial crisis and Housing bust.

02/2020 - ... -- the Pandemic-induced coma recession. An economic lockdown that prevented spending and other economic activity involving human interactions.

see: National Bureau of Economic Research (NBER)

Some economists believe that business cycles are combinations of 50 year "long waves" of economic activity and 7 year short waves occurring from short-term over expansion as defined above. These long waves or Kondratieff waves occur due to the presence and eventual saturation of broad investment opportunities. So far the U.S. has experienced 4 Kondratieff waves as listed below:

| Date | Wave | Reason(s) driving the expansion |

| measured: Trough-Peak-Trough | ||

| ____ to1790 to 1845 | First | Industrialization, Advent of steam power and development of the textile industry. |

| 1845 to 1870 to 1895 | Second | Growth fueled by investment opportunities of the westward expansion in the U.S. The building of canals and railroads. |

| 1895 to 1920 to 1940 | Third | Investment opportunities created by electrification of the U.S., emergence of radio and development of the auto, steel, and energy industries. |

| 1940 to 1980 to 2020 (??) | Fourth | Investment opportunities in the electronics, chemicals, plastics, medicine, telecommunications and information technology sectors. Financial Sector Reform. |

A Kondratieff cycle: A long wave of economic activity driven by demographics, innovation, resource discoveries and broad opportunities for investment.

The magnitude of the Great Depression is often explained as the combination of a severe short wave business cycle and the trough of the third long wave. The severity of the short wave may have occurred due to mistakes made in the execution of monetary policy by the Federal Reserve, the Smoot-Hawley Tariff Act, and the international breakdown of the gold standard as a fixed exchange-rate regime.

|

|