Over time labor markets are impacted in the long run by demographics, changes in productivity and the rate of growth in potential output. In the short run these markets will reflect volatility in the level of economic activity -- imbalances between the ability to spend and the ability to produce. In order to fully understand the employment picture we need to make use of two separate measures. One is the Unemployment rate which represents the ratio of those actively seeking work and the total number of people in the labor force. The other is the Labor Force Participation Rate which is a reflection of those entering or leaving the civilian labor force.

The Unemployment Rate: the percentage of those in the labor force actively seeking work.

An individual is considered to be Employed if she/he is working for pay at least on hour per week.

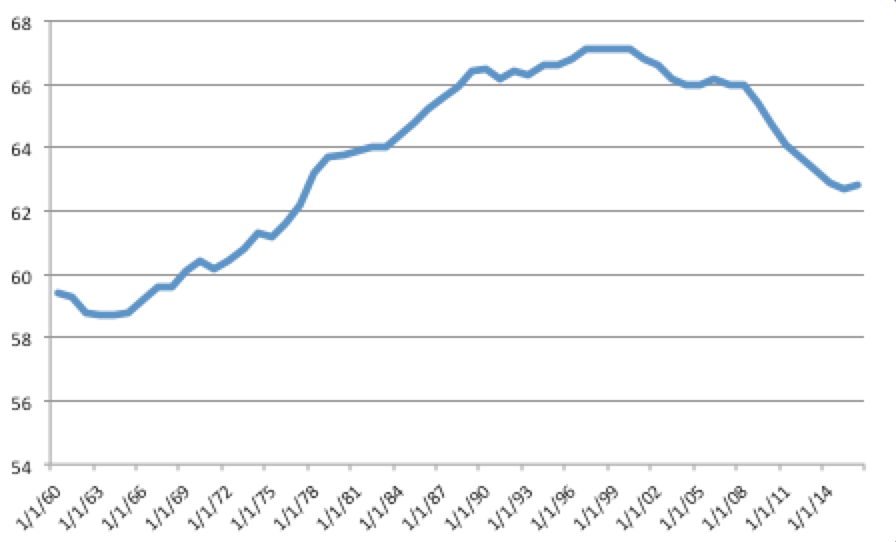

The Labor Force Participation Rate: the percentage of those available for work actually in the labor force

(working for pay or seeking work).

The following table aids in the understanding of how these values are computed.

| Category | 1990 | 2000 | 2010 | 2019 | |

| A. | U.S. Population (2019 est.): | 249,973 | 275,372 | 308,745 | 330,086 |

| B. . |

less those not available for work (students, children, institutional population): |

60,809 | 62,795 | 70,915 | 71,590 |

| C. | The Number of People available to the labor force: | 189,164 | 212,577 | 237,830 | 259,175 |

| D. . |

less those not working (retired persons, home caretakers...): |

63,324 | 69,994 | 83,941 | 95,636 |

| E. | The Labor Force: | 125,840 | 142,583 | 153,889 | 163,539 |

| F. . |

less those currently seeking work (the unemployed): |

7,047 | 5,692 | 14,825 | 6,001 |

| G. | Anyone working for pay in a given survey week (the employed): | 118,793 | 136,891 | 139,064 | 157,538 |

| Ratio | Measure | 1990 | 2000 | 2010 | 2019 |

| (E)/(C) | the Labor Force Participation Rate: | 66.5% | 67.1% | 64.7% | 63.1% |

| (F)/(E) | the Unemployment Rate: | 5.6% | 4.0% | 9.6% | 3.7% |

Frictional Unemployment represents those individuals that have left one job but are certain to begin their new job within a relatively short period of time. Often this type of unemployment accounts for those in-between jobs and is the result of individuals responding to market forces in the economy.

Structural Unemployment exists when broad structural changes are taking place in an economy such that certain job categories or skills are eliminated from labor markets. These changes may be the result of technological change, changes in tastes or preferences for particular goods, changes in the regulatory environment with respect to certain products (pharmaceuticals, tobacco, pesticides), or changes in any barriers to trade. Structural unemployment tends to be a long term phenomenon addresses by education and new training of those who are structurally unemployed.

Cyclical Unemployment occurs when individuals suffer job losses due to changes in the economic (business) cycle. Often as growth in economic activity reaches its peak and begins transition to a contraction, employers will begin to curtail production, to avoid additions to accumulating inventories, and thus begin to furlough a fraction of their workforce. In the rebounding period, from contraction to expansion, the opposite occurs as employers add employees to their payrolls and increase the rate of production.

The natural rate of unemployment is that rate where there is neither upward pressure nor downward pressure on the price level. If the actual rate of unemployment is below this natural rate, then labor markets are fairly tight making it difficult for firms to hire new workers. The quickest way to meet these hiring needs is to offer higher wages to either bid employees from other firms or to induce new workers to enter the labor force. However, since wages are a significant proportion of production costs, these costs will tend to rise putting upward pressure on output prices as firms attempt to protect profit margins. If the actual rate of unemployment is above the natural rate indicating a slack labor market, this pressure on wages does not exist.

The Natural Rate of Unemployment: that unemployment rate where there is neither upward pressure nor downward pressure on the price level

Historically the natural rate of unemployment (the value where policy makers view the economy at full employment is in the range of 4.5 - 5.0%

Labor markets can be divided into two groups of individuals -- those that are employed and the unemployed seeking work. In a market economy, it is common for workers to seek out the best employment-fit with their skills, initiative, employment preferences (place and type of work, hours and work environment), and salary expectations. Often, those in the pool of the employed will seek a change in the condition of their employment to find this best fit. As they leave one job, they become a job seeker, and upon finding new employment they are a job finder. Differences in the rates of job seeking and job finding will either swell the ranks of the unemployed or reduce the size of this group.

Both institutional and economic factors can influence these rates of job seeking and job finding. Institutional factors include the efficiency in the communication process between job seeker and potential employer, willingness on the part of the employee to accept less than perfect terms of employment, and the laws than govern the hiring and retention of employees. Economic factors can include, the items listed above related to changes in the business cycle (affecting the demand for workers) and structural conditions which may affect the match between the needs of employers and the skills that exist in the workforce.