Aggregate Supply represents the ability of an economy to produce goods and services. In the Long Run this ability to produce is based on the level of production technology and the availability of factor inputs. As stated earlier, production refers to the conversion of inputs -- the factors of production into desired output.

An aggregate production function is often written as follows:

Y*t = f(Lt,Kt,Mt )

where Y* is an aggregate measure of potential output in a given economy.

Over time with growth in the availability of factor inputs or technological improvement, the level of potential output increases. Thus in the Long Run we define the Aggregate Supply (ASLR) function as being influenced by those elements included in the production function and independent of the price level.

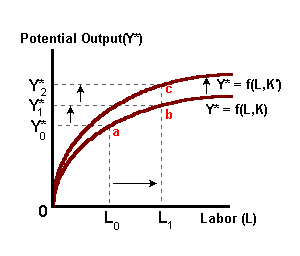

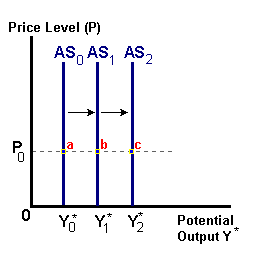

| Production | Long Run Aggregate Supply. |

|

|

In the above diagrams we find that in time period '0' the economy is capable of producing a level of output equal to Y*0 (point a). Growth in the amount of labor ('a' to 'b') available allows for the production of more output with existing levels of technology (Y*0 to Y*1). More capital (or materials) or improvements in productivity will lead to an even greater potential to produce (Y*1 to Y*2) at each-and-every price level (i.e., 'b' to 'c').